.png)

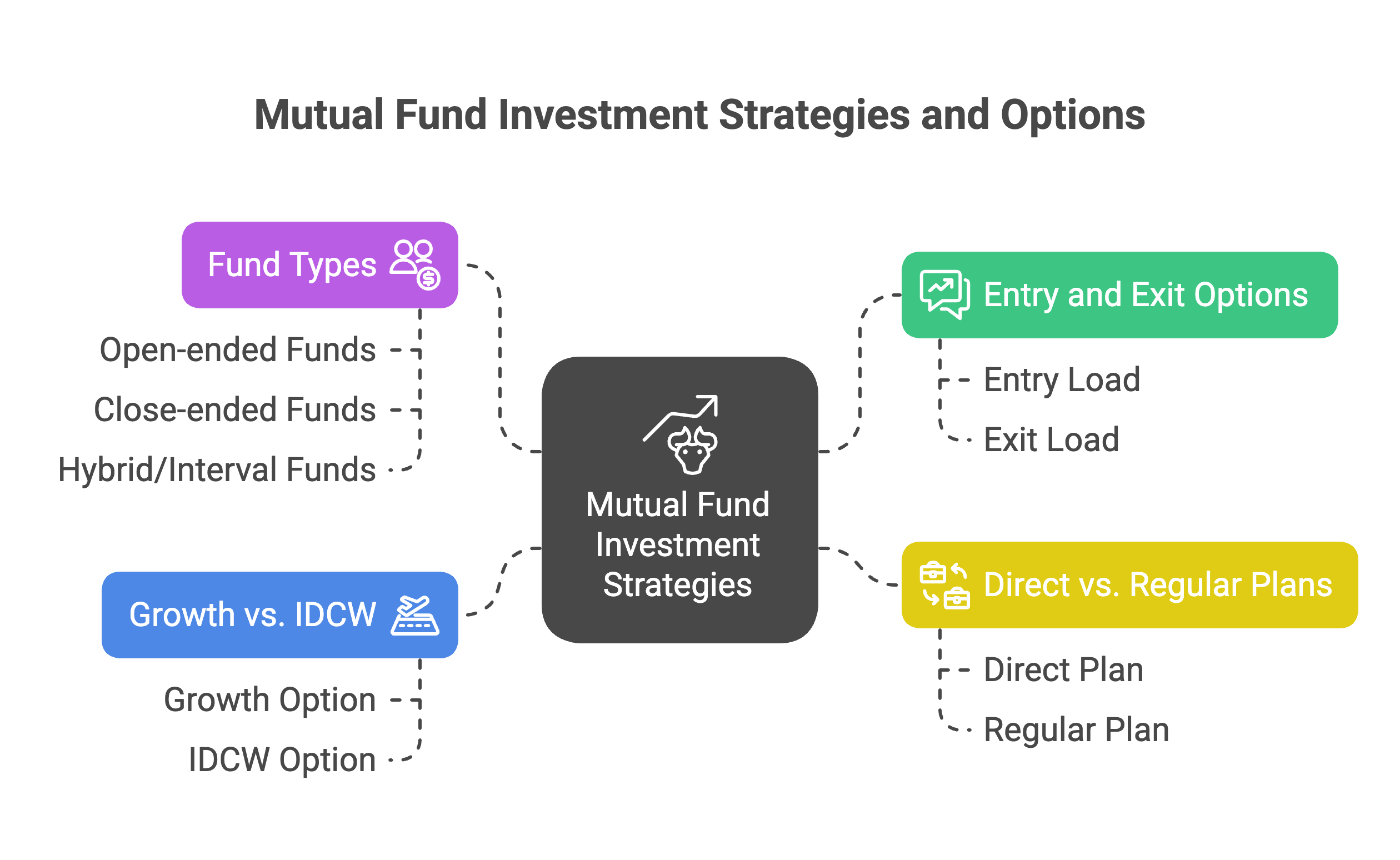

When it comes to building wealth through mutual funds, choosing the right fund is only half the journey. The other half is about how you invest and how you withdraw. Just like buying a house some people pay upfront, some pay in EMIs, and some increase their payments as their income grows mutual funds also offer flexible modes such as Lump sum, SIP, STP, Top-up SIP, and SWP. Each of these methods suits different financial situations, goals, and personalities. Understanding them helps you not only enter smartly but also exit gracefully, ensuring your money works for you at every stage of life.

Modes of Investment:

Lumpsum, SIP, STP, and Top-up SIP, SWP

Think of how people buy a house. Some pay the entire amount upfront (lumpsum). Some pay in monthly EMIs (SIP). Some shift money gradually from savings to home instalments (STP). Some start with a small EMI and increase it yearly (Top-up SIP).

Lumpsum: The “All at Once” Approach

A lumpsum is a single, one-time investment of a large amount. This method is straightforward and effective when you have a significant sum of money, such as an annual bonus, an inheritance, or from any selling a property.

-

Maximizes Compounding: Your entire sum is invested immediately, giving it the maximum possible time to grow and compound. Over long periods, this can lead to higher returns than a phased investment.

-

Capitalizes on Market Lows: If you have the knowledge and confidence to invest during a market downturn, a lumpsum investment allows you to buy units at a low price, setting the stage for significant growth when the market recovers.

-

Convenience: It’s a one-time decision. You don’t have to manage regular investments or recurring debits.

-

Individuals with a significant sum of money (e.g., a bonus, inheritance, or sale proceeds).

-

Investors with a high-risk tolerance who are confident in their ability to time the market.

-

Someone with a very long investment horizon who wants to put their money to work immediately.

Suresh, a software engineer, sells a small plot of land he inherited for ₹25 lakhs. He plans to use this money as a down payment for a flat in 5 years. Instead of leaving the entire sum in his savings account, he invests the full ₹25 lakhs into a dynamic bond fund. The goal is not high growth but to earn better returns than a fixed deposit while keeping the principal relatively safe. He chose a lump sum because he had a clear goal and wanted to put the entire amount to work immediately. So, 25 lakhs for 5 years with 7% rate of interest would be 35 lakhs so the total wealth gain will be 10 lakhs.

SIP (Systematic Investment Plan): The “Slow & Steady” Path

A SIP is a disciplined approach where you invest a fixed amount of money at regular intervals, such as monthly or quarterly. It’s not an investment product itself, but rather a method of investing.

How it Works: By investing a fixed amount, you buy more units when the market is down and fewer units when the market is high.

-

Disciplined Investing: An SIP automates your savings and investing, building a regular habit that separates your savings from your spending.

-

Rupee Cost Averaging: This is a key benefit. By investing a fixed amount regularly, you buy more units when the market is low and fewer units when it is high. This lowers your average cost per unit over time and reduces the risk of investing a large amount just before a market crash.

-

Accessibility: You can start an SIP with as little as ₹500, making it accessible to a wide range of investors.

-

Salaried individuals and regular income earners who can set aside a fixed amount each month.

-

Beginner investors who are new to the market and want a simple, low-stress way to start.

-

Anyone who wants to avoid the psychological stress of timing the market.

Preeti, a 25-year-old marketing executive, has just started her first job. She wants to start saving for her retirement, which is 35 years away. She knows she can’t invest a huge amount at once, but she can comfortably set aside ₹5,000 every month from her salary. She starts a monthly SIP in a diversified equity fund. Over the next few decades, her small, consistent contributions will benefit from compounding and rupee cost averaging, allowing her to build a substantial retirement corpus without ever feeling the pinch. So, she invests 5000 monthly for 35 years that would be 21 lakhs of total investment at 13% rate of interest her total value after 35 years would be 4,26,15,920 her wealth gain would be 4 cr.

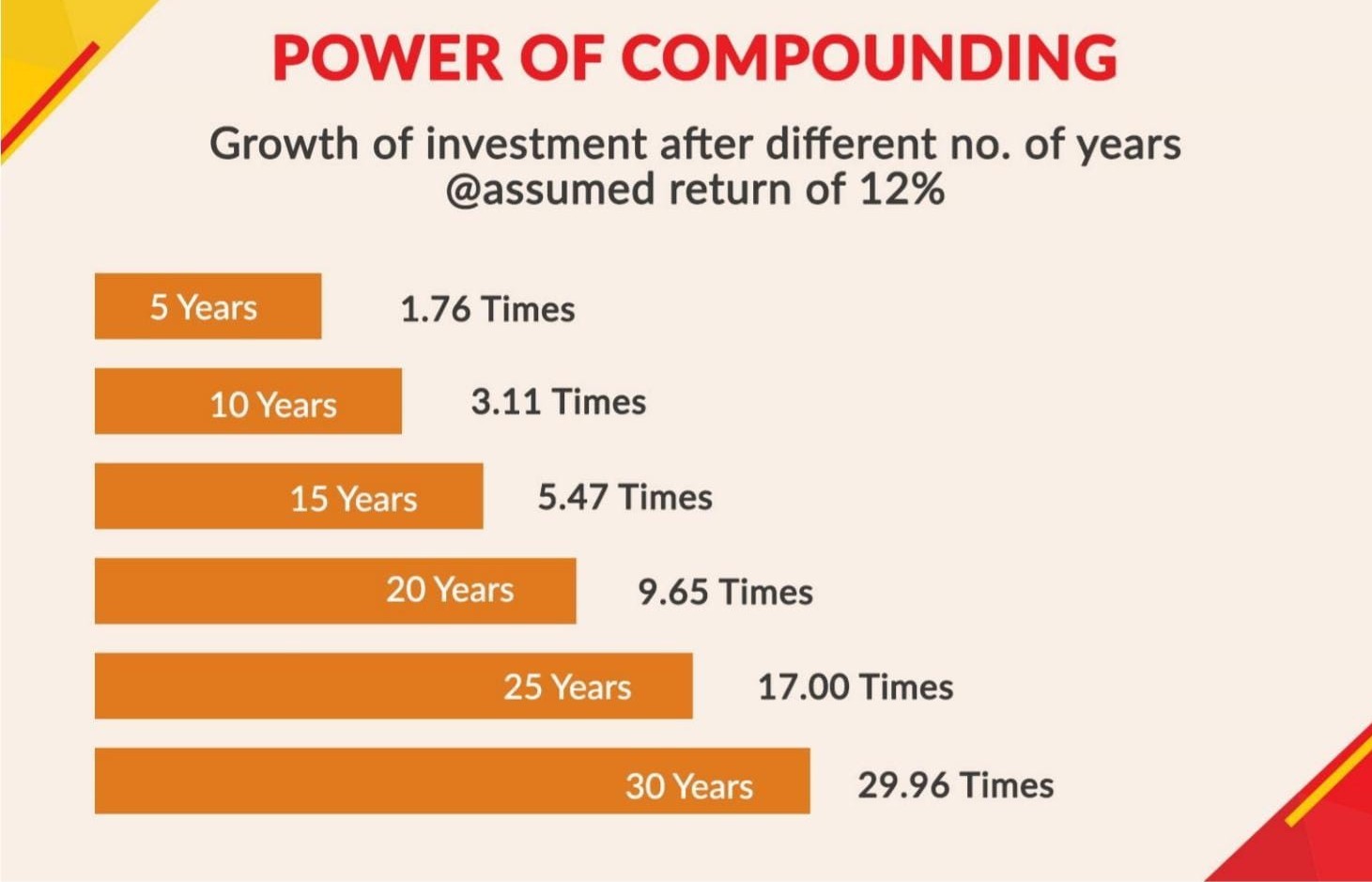

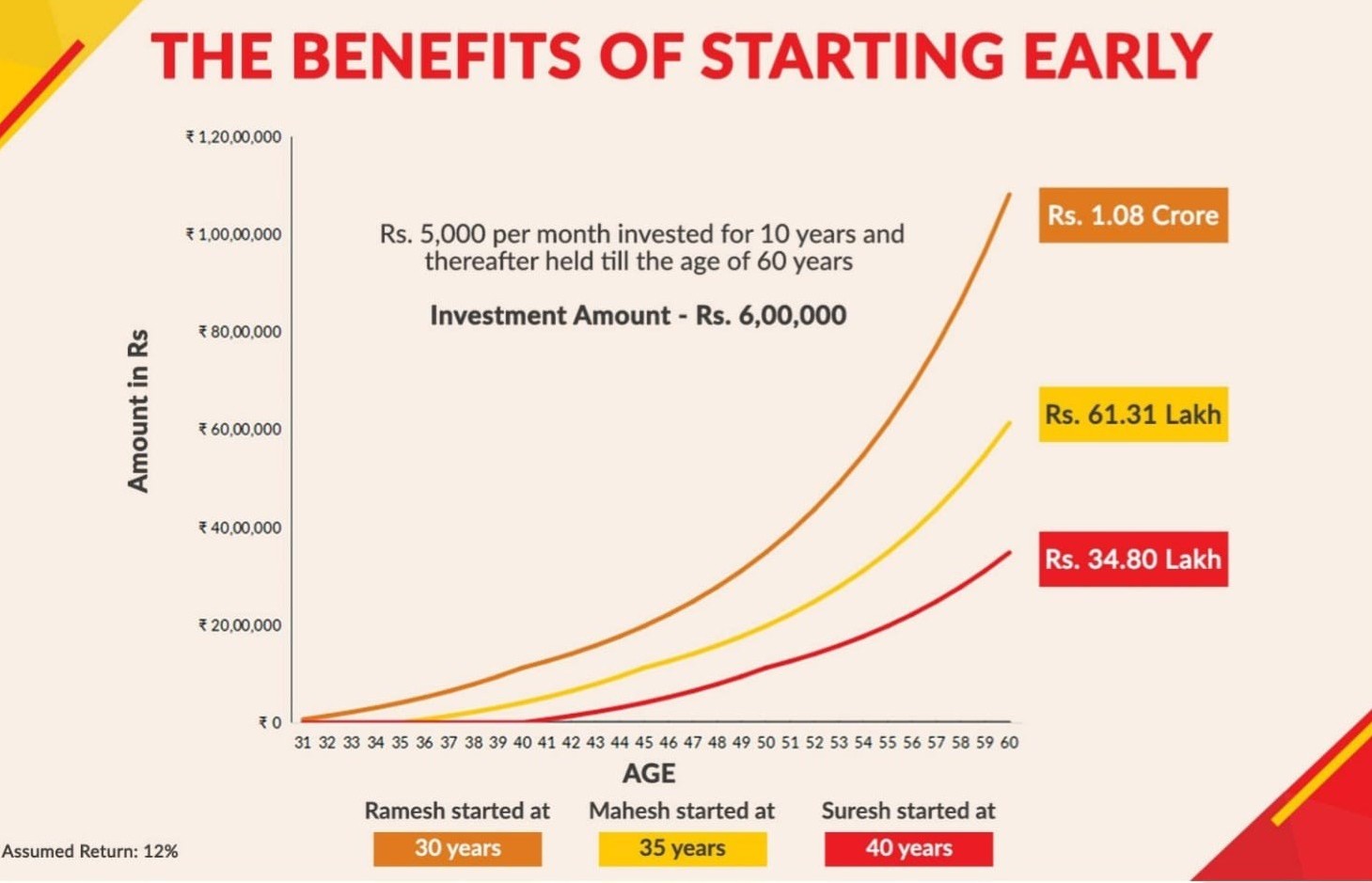

Also, we explained in our earlier blog on (reasons to choose Mutual fund) SIPs, that how starting early makes a huge difference. For example, Arjun invests ₹5,000/month for 35 years at 12% return through equity funds, his ₹15 lakhs grow to ₹95 lakhs, while in fixed deposits at 6% it would be far lower. This shows why mutual funds are a smarter choice for long-term wealth creation. click here

STP (Systematic Transfer Plan): The “Smart Move” Strategy

An STP allows you to transfer a lump sum from one mutual fund scheme to another within the same fund house. It’s designed to manage risk.

This is the perfect solution if you have a lump sum but are worried about a sudden market drop. You can park your money in a relatively safe fund (like a liquid fund) and transfer it systematically into a more volatile one (like an equity fund).

-

Manages Market Risk: STP combines the benefits of a lumpsum and an SIP. It allows you to invest a large sum gradually, mitigating the risk of a single-entry point.

-

Earns Returns on Parked Funds: While you are gradually transferring money to an equity fund, the remaining lump sum is parked in a low-risk debt fund (like a liquid fund) where it continues to earn returns, rather than sitting idle in a savings account.

-

Flexibility: You can choose the amount and frequency of your transfers, tailoring the plan to your risk comfort level.

-

Individuals with a large lump sum who are cautious or worried about market volatility.

-

Investors who want to transition from low risk to high-risk investments in a controlled, systematic manner.

Ramesh, a 45-year-old businessman, gets a ₹20 lakh refund from an old investment. He wants to invest this money in equity markets for his child’s higher education, but he is nervous about a potential market correction. Instead of a lumpsum, he parks the entire ₹20 lakhs in a liquid fund. He then sets up an STP to systematically transfer ₹50,000 to an equity fund on the 10th of every month. This way, his money earns a small return in the liquid fund while he slowly enters the volatile equity market over a period of 40 months.

Top-up SIP: The “Level-up” Feature

A Top-up SIP, also known as a Step-up SIP, is a feature that automatically increases your SIP instalment amount at predetermined intervals.

This is ideal for salaried individuals who expect their income to increase annually. It ensures your investments keep pace with your rising income and personal goals.

You set the amount or percentage by which your SIP will increase, and the fund house does the rest.

Benefits:

-

Beats Inflation: By systematically increasing your SIP amount, you ensure your investments grow faster than the inflation rate.

-

Matches Your Income Growth: This feature automatically aligns your investments with your salary hikes, ensuring you’re saving more as you earn more.

-

Accelerates Goal Achievement: By investing more over time, you can reach your financial goals (like a down payment on a house or a retirement corpus) much faster than with a standard SIP.

Best For:

-

Young professionals who expect their income to grow steadily.

-

Anyone with long-term financial goals who wants to maximize their wealth creation over time.

Example: The Ambitious Careerist:

Anjali, a 30-year-old project manager, starts a monthly SIP of ₹10,000 to save for her daughter’s college fund for 20 years. She predicts an annual salary hike of around 10%. To make her savings keep pace with her income, she opts for a 10% annual Top-up SIP. This simple action means that in the second year, her SIP becomes ₹11,000; in the third, it’s ₹12,100, and so on. Without any extra effort, her investment contributions grow automatically, ensuring her corpus grows much faster than a standard SIP. So, her total investment is of 68 lakhs, total after 20 years will be 2,21,78,821 and her wealth gain will be 1,53,05,821.

SWP (Manages Market Risk Withdrawal Plan)

Once you’ve built your corpus, you need a smart way to exit.

It Allows you to set up a regular withdrawal amount from your investment, like a pension. This is ideal for retirees.

Benefits:

-

Creates a Regular Income Stream: The primary benefit of an SWP is to provide a steady, predictable cash flow, which is crucial for those no longer in the earning phase.

-

Allows Remaining Corpus to Grow: Unlike redeeming your entire investment at once, an SWP only sells the required number of units to meet your withdrawal amount. The rest of your corpus remains invested and continues to benefit from market growth.

-

Tax Efficiency: An SWP can be a more tax-efficient way to withdraw money compared to other income sources like bank FDs, as capital gains are taxed only on the withdrawn amount.

Best For:

-

Retirees and senior citizens who need a regular income to cover their living expenses.

-

Individuals who have built a large corpus and want to start drawing from their investments without liquidating their entire portfolio.

Example: The Retired Couple

Mr. And Mrs. Sharma, both retired, have a mutual fund corpus of ₹1.5 crores. They live on a pension, but they need an additional income of ₹50,000 per Year to cover their expenses and travel. They set up an SWP to withdraw this amount every year from their hybrid mutual fund. This strategy provides them with a steady income while the remaining ₹1.5 crore continues to stay invested and grow in the fund, ensuring their money lasts for the rest of their lives.

Since, there is no single “best” way to invest or withdraw the right choice depends on your goals, time horizon, and risk appetite.

Lumpsum works best when you have a large amount ready and want immediate growth.

SIP is the tried-and-tested way to build wealth gradually, perfect for salaried professionals.

STP helps cautious investors enter volatile markets smartly.

Top-up SIP ensures your investments keep pace with your rising income and inflation.

SWP is the ideal exit strategy, providing a steady income stream in retirement without exhausting your wealth.

Invest smartly, withdraw wisely, and let mutual funds become your lifelong wealth partner.

Note (Please Read)

Mutual funds are subject to market risk. Read scheme documents (SID/KIM/factsheet) carefully. Past performance does not guarantee future results. Choose funds that match your goals, time frame, and risk tolerance.

.png)

.png)

.png)

.png)